Part 3/4: Secured vs Unsecured Debt and Understanding Subordination

So you want to borrow money for your growing startup? In part 3 of our discussion on debt, we discuss the importance of secured and unsecured debt and how subordination comes into play as you add debt holders to your current list of equity investors.

Here’s an overview of key considerations:

Balancing Secured and Unsecured Debt:

- Secured debt offers easier access to financing, flexible terms, and lower interest rates by providing collateral, such as company assets, property, or accounts receivable. However, defaulting on secured debt poses the risk of losing valuable assets.

- Unsecured debt, although more challenging to secure, eliminates the risk of asset loss. Lenders charge higher interest rates and impose stricter repayment requirements due to the increased risk.

Assets Considered for Securitization:

- Equipment and Machinery: Valuable equipment or machinery can be securitized, bom

One important note: Most startups will be in a net burn situation and a growing company may resort to financing based on future Annual Recurring Revenue (ARR) when traditional metrics like EBITDA are not yet meaningful.

ARR financing is used for SaaS companies where subscription-based services generate reliable recurring revenue, and there is an understanding that a nascent business with significant startup costs can scale up quickly.

ARR financing documents are similar to traditional leveraged documents, but instead of relying on EBITDA, they utilize leverage tests based on ARR. (Lenders are smart and they will take out Maintenance, consultancy, or service fees from your ARR calculations).

ARR leverage tests are used to make sure that you don’t go over a threshold and can service your debt. There may also be a liquidity covenant to ensure the company has sufficient cash reserves to handle potential performance challenges and adjust its workforce if needed (since the headcount will typically be the biggest component of your cost).

ARR financings often incorporate Payment-in-Kind (PIK) toggles to accommodate cash constraints during the initial growth phase. The loan agreement typically includes a “flip” provision, transitioning from the ARR leverage test to a traditional EBITDA leverage test after a specified period, typically two to three years. This aligns with the company’s projection of achieving substantive profitability in the future.

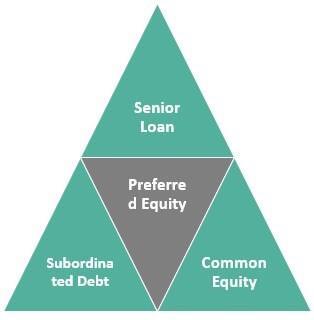

Understanding Subordination:

- Lenders play a crucial role in determining the prioritization of creditors’ claims in subordination. Senior lenders are typically repaid first in bankruptcy scenarios, protecting their higher priority status.

- Subordination helps lenders manage risk by providing senior lenders with priority access to assets and cash flows. Senior lenders may have a first lien on specific assets, such as real estate or equipment, ensuring a more secure position for repayment.

- The subordination hierarchy impacts a company’s capital structure and attracts different types of investors. Senior debt may be more appealing to conservative investors seeking lower risk, while subordinated debt may attract investors looking for higher returns.

- Subordination terms are outlined in legal agreements and significantly impact lenders’ risk exposure and repayment prospects. Intercreditor agreements specify the rights and priority of different lenders, ensuring clarity in default or bankruptcy scenarios.

- Dont skimp on the legal review of loan documents, it’s super important to understand the fine print and make sure you understand all the covenants and details.

Don’t Go Crazy with Debt

Think of the situation when you are about to raise a Series C round and the equity investors find all this debt on your balance sheet. A reasonable amount is fine (and it might not matter if your company is performing well), but no one wants to give you money to service your debt, so think it through and make sure your overall capitalization makes sense.

Costs of Debt:

- Debt costs vary based on factors such as risk assessment, creditworthiness, collateral requirements, market conditions, loan maturity, repayment terms, and lenders’ risk appetite.

- Lenders assess the risk involved in providing debt financing and may charge higher interest rates or additional fees for higher-risk borrowers.

- Companies with strong credit profiles and reliable cash flows are seen as lower-risk borrowers, often receiving more favorable interest rates and terms.

- External market conditions, including interest rate fluctuations impact the cost of debt.

- Longer-term debt generally carries higher costs compared to shorter-term debt, and repayment terms and associated fees also influence the overall cost.

- Different lenders may have varying risk appetites, leading to different costs of debt based on their perception of risk.

Once again, read the fine print and negotiate with your lenders, and don’t go crazy with debt.

Check out ,Part 4 of 4 on our Series on Debt: “Revolver vs. Term Loan, How to Decide“.

Make sure you have not missed anything on this journey of “Understanding Debt Financing “.