Part 1 of 4: Surviving Your First Audit

As you scale and add more financing, it will be time to prepare for your first audit. I typically push back on banks when they require an audit as it’s a major undertaking. There comes a point however when you are seeking a large facility (think $150M), that’s it’s time to get things in order for an audit.

There are many mistakes you can avoid in terms of getting your first audit completed. We’ve included a checklist to get started in this four-part series on getting through the audit process. One big lesson I’ve learned is to communicate. Ensure that both parties are aligned regarding expectations, timelines, and responsibilities. And it’s a long-term relationship you are developing with your audit partner. Ending an auditor relationship on a bad note will cause you quite a bit of problems so be thoughtful about picking the right partner and building on the partnership.

Step 1: Determine when you need an audit

You’ll need to complete an audit if you have investors and outside stakeholders to report, or if you’re preparing for an exit event. Your board may also request an audit report to ensure no material misstatements in the accounting records. Usually, the audit is triggered when you are raising a major round of financing (equity or debt) or getting ready to go public.

Step 2: Choose your auditor

Investors generally prefer the Big Four but smaller firms will give you more flexibility if you are an early-stage company. Mid-sized audit firms can offer more substantive support if you’re still in the process of establishing your controls and documentation. Make sure you meet your auditing team and request any specific experience that will be relevant to your specific industry.

Finding the Right Partner and Getting Started

The most important decision you’ll make is deciding which audit team to work with. You are establishing a long-term relationship with your auditors and just like you would with a new employee, you need to assess and grow your comfort with your auditors.

Meet the entire audit team before they start their work. You’ll receive the pitch deck with all the work that the auditors have performed in the past so go through it ahead of time and have your questions prepared. Understand their expertise and their experience serving clients in your specific industries.

Be proactive about asking for people with experience in auditing and accounting knowledge related to your industry. Someone who is an expert in the manufacturing industry is not going to fit your growing SaaS cybersecurity company, and if you’re doing consumer neo-banking as a fintech startup, you will need the right expertise so it’s not a learning exercise for them.

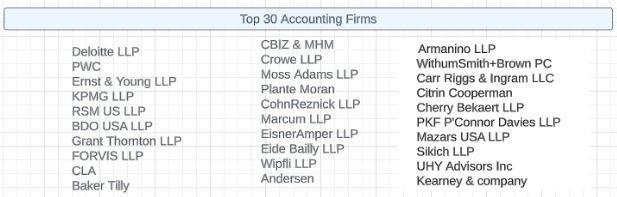

Here’s a list of the top 30 accounting firms but there are thousands more so do your due diligence or ask for a referral.

These are the top auditors that are used often by my CFO colleagues.

- BDO USA, LLP

- RSM US LLP

- Grant Thornton LLP

- Crowe Horwath LLP

- CBIZ MHM, LLC

- Baker Tilly US, LLP

- CohnReznick LLP

- CliftonLarsonAllen LLP

- Moss Adams

- EisnerAmper

- Marcum LLP

Step 3: Set parameters for working together and do the early prep work (You are paying the bills)

In your audit kickoff meeting, establish a timeline and communication workflows. Make sure everything funnels through you. Verify how you’ll be sharing files and that your documents will be stored in a secure location. Go over the timeline for when your Prepared by Client (PBC) documents will be ready to be shared in Dropbox.

Do the Prep Work Ahead of Time before the Kick Off

The first audits are always extremely time-consuming because they require a lot of data cleanups, review, back and forth, and accounting reclassification. Gather all needed resources and compile essential documents. You’ll need the support of everyone in your organization to complete the audit. Prepare them for the audit by detailing expectations and outcomes.

- The R&D Team. Engineers or the CTO would provide you with details for your IP capitalization and R&D tax credits.

- The IT Manager will provide all the software tools and internal control systems that you use.

- Sales will explain the details of sales contracts so have all the contracts in Dropbox ready to go. The big issues that come up is revenue contracts with customers so get a head start by reviewing all the paperwork.

- Customer success should have customer communications documented

- HR will provide support for salaries, bonuses, and other information.

Reminder, auditors will not tell you the materiality threshold used for the audit, but you can come up with a number that you are comfortable with as you prepare. Perform an internal review of all accounts and ensure that there are no differences that cannot be reconciled with appropriate support.

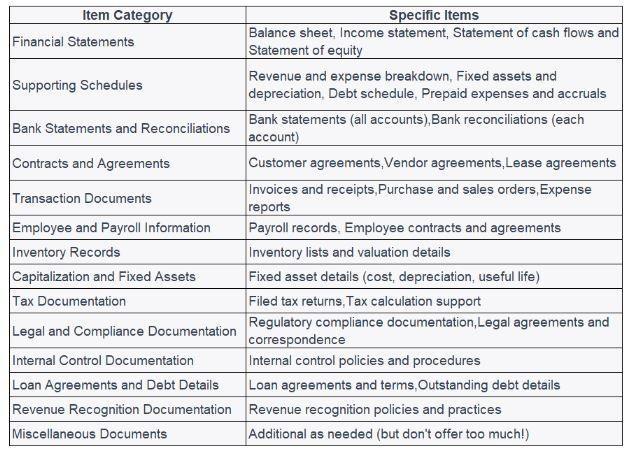

Step 4: Compile all the important documents for the audit

This growing list of required documents will include:

- Corporate documents, minutes for all board meetings, and significant agreements

- Reconciliation for all accounts with a balance over your internal materiality

- Support for all significant transactions

- List of contingent liabilities

- Revenue recognition memo documentation

- Draft financial statements with notes

- List of subsequent events

Not Just Numbers, Confidence in the Numbers

The goal of the auditors is to assure your stakeholders that your finances and accounts are in good order, and, more importantly, that they can trust your numbers and that things are done correctly. Remember, you are spending close to $80,000 or more for your first audit (depending on the scope) so be thoughtful of having everything ready to go and give the auditors the confidence that you have things in order.

Discuss and outline the process and lead with full ownership of the audit process.

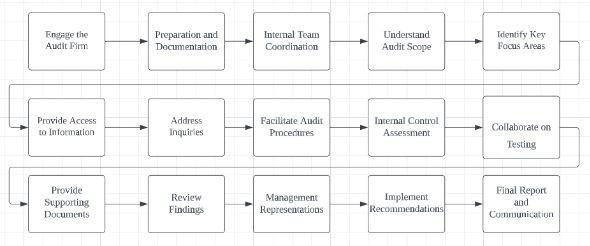

Audit Process

Cleanup all your Working Papers

Auditors will scrutinize everything you share with them. During your first audit, everything that your team sends should go through you so you can make sure you review these documents for any red flags, outstanding issues that need to be resolved, broken links, and inconsistent formulas. Understand what’s relevant to the audit and remove everything else, e.g. extra tabs in your Excel worksheets, extraneous calculations, and links.

Your auditors should never be emailing your CEO or other team members outside of finance and accounting directly. Always ask for an agenda in advance of any meetings or calls so you can adequately prepare your team. Steer the process and direct the initiative.

Get Stuff in Order (PBC, Provided by Client)

Less experienced controllers often look to auditors to help them determine what level of documentation is needed to validate their accounting policies. Be assertive, take a position on accounting policies, and be clear about the control environment even if it is non-existent. Hesitation and ambiguity are big red flags for auditors so be prepared.

PBC documents and files

Expect to prepare multiple drafts, reviews, and rewrites of the financial statements. Make sure that the early drafts are reviewed by your executive team and legal counsels and that they are comfortable with the notes related to related parties, contingent liabilities, and subsequent events.

Our next chapter deals with leading the audit process and getting ahead of complex issues that inevitably come up.